19 DECEMBER 2018

What tax changes are in the pipeline for 2019?

Parliament has finished their sittings for 2018 and the next sitting will be on 12 February 2019.

Some tax proposals not yet enacted, include:

- Changes to the integrity measures to determine whether a company can use tax losses from previous years (e.g. new “similar business test” concept);

- Removal of main residence exemption for foreign residents;

- R&D tax incentive changes; and

- Various superannuation changes.

The passing of any new legislation any time soon will be a difficult balancing act, not just because of the different opinions of different political parties, but also because of tight timeframes (e.g. the 2020 Budget is scheduled to be delivered on 2 April 2019 and the Federal election is to be held prior to 18 May 2019).

Nevertheless, Nexia Australia Tax will keep you updated about all these proposed changes through independent analysis of the impact they may have for our clients.

31 OCTOBER 2018

Outstanding tax debt? We can help you set up a payment plan

We would strongly encourage any business with current outstanding tax debts to engage with your Nexia representative to ensure outstanding tax debts are paid in a timely and affordable manner. We can assist a business with establishing a payment plan with the ATO to avoid or minimise penalties and late interest charges on outstanding tax debts, or alternatively your Nexia representative can arrange solutions to refinance and restructure your debts, in order to manage your cashflow.

With an ATO payment plan to manage existing debt, you still need to lodge all of your ongoing activity statements and tax returns and the ATO will expect tax liabilities arising from those lodgements to be paid on time.

8 AUGUST 2018

Are you entitled to claim fuel tax credits?

Please ensure that fuel tax credit (FTC) claims are made at the correct rate because the fuel tax credit rates have increased from 1 August 2018. FTCs are calculated on the amount of fuel tax payable and the type of fuel (petrol, diesel, kerosene, blended fuels) used. FTCs are available for vehicles with a gross vehicle mass exceeding 4.5 tonnes that travel on public roads. FTCs may also be available for eligible business usage of machinery, plant, equipment and light vehicles travelling off public roads or on private roads. Simplified fuel tax credit rules apply for claims of less than $10,000.

We would be pleased to assist with making FTC claims as well as reviewing whether correct rates for claiming FTCs have previously been used.

11 JULY 2018

More tax information on cryptocurrencies

As mentioned in previous top tax tips, cryptocurrencies held as investments will be treated as CGT assets (as opposed to money or currency) and any gain on disposal will be taxed under the concessionary CGT regime (i.e. qualify for the 50% CGT discount if the cryptocurrency has been held for 12 months or more).

However, on the disposal of cryptocurrencies that are personal use assets (e.g. if use of cryptocurrencies is mainly to purchase items for personal use or consumption):

- Capital gains will only be recognised if the cryptocurrency was originally acquired for $10,000 or more; and

- Capital losses will be disregarded

Cryptocurrencies acquired in a profit-making scheme or in the course of carrying on a business will be treated as trading stock (i.e. if the value of the closing stock at the end of the year is more than the opening stock at the beginning of the year, the difference must be included in assessable income).

4 JULY 2018

Beware of tax time scams

During tax time, there is usually a sharp spike in the number of email and telephone scams doing the rounds (e.g. a fraudster, claiming to be from the ATO, may call you and request some personal information or demand payment of an outstanding tax debt).

If you receive any such suspicious phone calls (or emails) claiming to be from the ATO, please do not provide any information. The ATO does not send people emails requesting the payment of debts. We would strongly suggest that you hang up immediately (if contacted by phone) and contact us as soon as possible so that we can bring this to the attention of the ATO.

Please also be aware that your Nexia advisor can, at any time, ascertain what taxes are owed and the relevant payment date(s). If you are unsure about the amount of tax you owe, please check with your Nexia advisor before payment.

20 JUNE 2018

Reminder of some of the main tax changes for 2018

When applying the tax law detailed consideration must be given to a person’s or entity’s circumstances. This process cannot be simply following a generic checklist and ticking boxes (a practice unfortunately rife in many firms) or doing exactly what was done the year before. Tax and superannuation laws are constantly changing such that the application of the law in one year may be different in a subsequent year. For this reason, checking with your Nexia advisor on how the law will apply to the transaction is important when embarking on a significant transaction.

Set out below are some of the main brand new tax changes that affects the 2018 income tax year:

- 27.5% company tax rates for companies carrying on business with a turnover of less than $25 million – as per the current law as at the date of this top tax tips;

- No more budget repair levy (so top marginal tax rate is 47%);

- No more travel deductions to inspect residential rental properties;

- Limited depreciation deductions on previously used plant and equipment in residential rental properties;

- 12.5% foreign resident CGT withholding tax (and a $750,000 threshold);

- First year of first home super saver scheme to enable taxpayers to buy their first home [i.e. can make superannuation contributions to a maximum of $15,000 (if single) and $30,000 (if couple) in 2018];

- Superannuation contributions of individuals earning income of more than $250,000 will be taxed at 30% and payable by the individual although the individual can complete a release authority to obtain reimbursement from their superannuation fund;

- Salaried workers can now claim a deduction for personal superannuation contributions.

SME businesses should also consider whether they can qualify for:

- Small business entity concessions (e.g. $20,000 instant asset write-off, small business restructure rollover, simplified depreciation and trading stock rules etc.) – for businesses with a turnover of less than $10 million; or

- Small business CGT concessions on the sale of the business – for businesses with a turnover less than $2 million or net assets of less than $6 million.

Please see our tax year-end planner for a more detailed discussion of the various issues to consider for the 2018 tax time.

13 JUNE 2018

Almost time for Single touch payroll (STP)

As reported in various previous top tax tips and our Tax Update, single touch payroll (STP) is due to start on 1 July 2018 for businesses that employs 20 or more employees as measured on 1 April 2018. Under the STP system, employees’ salaries and wages, PAYG withholding and superannuation information will be automatically reported to the ATO through the employer’s payroll software.

However, businesses involved in seasonal activities such as harvesting that only employs 20 or more employees for a short time in the year (that incidentally includes 1 April 2018), can be exempted from STP reporting if the seasonal employer:

- had fewer than 20 employees for 10 of the previous 12 months;

- will have fewer than 20 employees for 10 of the upcoming 12 months; and

- is not part of a wholly-owned group (e.g. if one of the companies is owned 100% by another company).

Please talk to us (especially if you are likely to have 20 or more employees at 1 April 2018) so that we can assist you to choose a payroll service provider that is STP enabled to ensure your payroll software is STP compliant by 1 July 2018.

30 MAY 2018

Year-end tax planning: 30 June 2018 is a Saturday this year. By when do you need to do what?

We are in the process of finalising our 2018 Nexia Tax year-end planner to inform small to medium businesses and individuals what the most important issues are to consider when doing their year-end tax planning (keep an eye on our website as the Planner will be published there soon).

One interesting procedural matter this year is that because 30 June 2018 falls on a Saturday this year, ATO payments or lodgements due on that day or on Sunday 1 July can be made on Monday 2 July 2018 without incurring a general interest charge. if at all practically possible, all actions, payments or lodgements should be undertaken before Friday 29 June 2018.

However, we would recommend that for actions that must be undertaken by 30 June 2018 such as qualifying for a deduction for superannuation contributions, that those contributions be received by the superannuation fund well before 30 June; contributions not in the superannuation fund’s bank account by 30 June will not be eligible for a tax deduction. Trading stock must also be valued on 30 June; detailed records must be retained of the stock taking process for at least five years.

16 MAY 2018

What effect will the recent Federal Budget have on you and your business?

The Federal Budget was delivered on 8 May 2018 and contained some proposed changes that, if enacted, will affect the following entities in the following ways for the 2019 income tax year (i.e. from 1 July 2018):

- Individuals: new $530 low and middle income tax offset and increase in the top threshold of the 32.5% marginal tax bracket from $87,000 to $90,000;

- Businesses: extend until 30 June 2019 the $20,000 instant asset write-off and some research and development (R&D) incentive changes; and

- Superannuation: a measure to prevent individuals who earn more than $263,157 per year from working more than one job from breaching the $25,000 concessional contributions limit and more strenuous enforcement on members of superannuation funds to lodge a notice of intent to claim a tax deduction for concessional (deductible) contributions.

The Government is also on the war-path against Phoenix activities. Directors of companies who leave companies incapacitated to pay their tax and other debts will be personally liable for avoided income tax, GST and luxury car tax. Unfortunately, the Budget papers do not announce a commencement date for this measure, but hopefully the measure will swiftly be enacted to shut down this economically harmful activity.

Furthermore, from 1 July 2019, businesses operating in the cash economy that make payments of more than $10,000 for services or goods must do so by direct debit, BPAY or cheque.

Please see our Nexia Budget summary here for a more detailed (but still concise) overview of the Budget.

Our Budget summary is easy to read and sets out in a practical manner:

- What the proposals are;

- How the proposals may affect you; and

- From what day the proposals are supposed to apply.

2 MAY 2018

Trading names will soon be a thing of the past

Businesses are reminded that from November 2018, only registered business names (as distinct from trading names) will be listed in ABN lookup.

Therefore, businesses will only be able to keep on trading under their current trading name if they register that trading name with the Australian Securities and Investments Commission (ASIC) before November 2018.

11 APRIL 2018

Lodge your 2017 research and development (R&D) claims by 30 April 2018

Certain companies can claim a tax offset for expenditure incurred on R&D activities. The aim of this offset is to encourage companies to invest in R&D work to create new or improved materials, products, devices, processes and services.

Lodging your claim on time may give rise to the following benefits for you:

- a cash injection (e.g. a cash rebate equal to 43.5% of the amount spent on R&D activities) for companies that have a turnover of less than $20 million a year; or

- a non-refundable tax offset of 38.5% for companies with a turnover of $20 million or more a year (i.e. the offset reduces tax payable and therefore can only be used in years the company has taxable income).

The deadline for the lodgement of the 2017 R&D tax concession claim with AusIndustry (a division of the Department of Industry, Innovation and Science) is 30 April 2018 and if this deadline is missed the company is not eligible for a R&D claim. We can assist you with lodging your claim.

We will be releasing an alert on the R&D incentive in due course. Next time you visit the Nexia website (www.nexia.com.au), please keep an eye out for this alert to identify potential R&D opportunities that may be available for you.

28 MARCH 2018

PAYG instalments: To vary or not to vary?

The PAYG instalment system (i.e. the system for making regular payments towards the expected annual income tax liability of a taxpayer) only applies to businesses or individuals earning business and/or investment income above a certain amount.

The ATO calculates the PAYG instalment rate based on the information reported on the latest tax return and if this calculated rate results in too much tax being paid, the business or individual will receive a refund of any overpayment once their tax return is assessed. Conversely, if insufficient PAYG instalments have been paid, a tax liability for the difference will arise.

If a taxpayer’s circumstances change in the current income year compared to the information in the prior year’s tax return (e.g. a current year may not be as profitable as the previous year) the taxpayer may want to lower their PAYG instalments for the current year.

However, if such a downward variation results in a greater than 15% shortfall of the actual amount of tax payable when the current year’s tax return is assessed by the ATO (i.e. there was an underestimate of the instalment rate or amount for the current year), the taxpayer may be subject to the general interest charge (GIC) on the difference. Therefore, a reasonable degree of certainty of the changed circumstances must exist before varying the ATO’s PAYG instalment rate.

As a general observation, most people prefer to pay PAYG quarterly instalments as they earn their income similar to an employee who has PAYG withholding tax deducted from their salary. The benefit of the PAYG instalment and withholding systems is that a large tax bill at the end of the income year, and the consequent need to find the cash to pay the bill, is avoided.

We recommend that you contact us before varying a PAYG instalment to avoid unnecessary penalties.

28 MARCH 2018

Tax treatment of cryptocurrencies

Cryptocurrency (i.e. a digital asset where encryption techniques are used to regulate the amount of units) is currently a big buzzword in Australia.

Because a cryptocurrency is treated like a CGT asset (as opposed to money or currency), a CGT event will occur when a cryptocurrency is disposed of and tax will have to be paid on any capital gain made on the disposal of such a cryptocurrency bought as an investment.

Taxpayers need to keep proper records (e.g. the date of the transaction, the value of the cryptocurrency a time of the transaction and what the transaction was for and who the other party was) in relation to such cryptocurrency transactions.

21 MARCH 2018

Single touch payroll: What is all the fuss about?

Recently, we published a Tax Update on the latest Single Touch Payroll (STP) developments.

Please read this alert to find out what you can do to ensure your business is STP ready by 1 July 2018 (i.e. either use a payroll provider that is STP ready or ask Nexia to assist you with your payroll function).

Because the ATO will have instantaneous access to payroll information through STP reporting, it is now more important than ever to avoid unnecessary errors when doing a payroll run. Nexia can help you implement strategies to avoid common payroll mistakes by ensuring employees are paid correctly, employees super entitlements are calculated correctly, overpayments are addressed correctly, and that employee information (e.g. names, birth dates and addresses) is correct.

28 FEBRUARY 2018

Reminder: 12.5% withholding tax may apply to properties sold this year

From 1 July 2017, all purchasers of certain types of Australian property (whether purchased from a resident or foreign resident vendor) must withhold 12.5% of the purchase price, unless:

- the transaction is excluded from these rules (e.g. properties sold for less than $750,000); or

- the parties undertake certain actions before settlement date (e.g. obtain an ATO clearance certificate, residency declaration or apply for a variation of the withholding rate).

Note, for the year 1 July 2016 to 30 June 2017, the CGT withholding rate was 10% and no withholding tax was payable on properties costing less than $2 million.

Please note that the application of this 12.5% withholding rule is not just limited to purchases but applies to all acquisitions (e.g. a transfer of relevant property through a gift, divorce proceedings or other distributions such as in specie property distributions from trusts or from deceased estates).

This effective 12.5% prepayment of the vendor’s CGT liability to the ATO will be allowed as a credit against the vendor’s tax liability when the vendor lodges their tax return.

Please let us know if you are thinking of buying real estate and know or suspect that the vendor is a foreign resident or has a foreign connection. Also, even if you are a resident vendor, we can help you to obtain an ATO clearance certificate or residency declaration so that the 12.5% withholding rule will not apply to you.

21 FEBRUARY 2018

Transition Issues: The Single Touch Payroll System

The streamlined STP reporting system – which will apply from 1 July 2018 to employers with 20 or more employees at 1 April 2018 - will report payments such as salaries and wages, allowances, deductions, other payments, pay as you go (PAYG) withholding and superannuation information directly to the ATO at the same time the employer pays employees.

The STP reported information will then be used to pre-fill business activity statements – obviating the need for employers to provide the following reports in respect of STP reported information:

- payment summaries to individuals; and

- payment summary annual reports to the ATO.

Because information not reported or captured in the STP system will still need to be reported on payment summaries, we would recommend that employers report as much allowable information as possible through the STP system.

Please speak to your Nexia Adviser to find out what information can be reported through STP and what information is excluded from STP reporting.

21 FEBRUARY 2018

Electronic data matching: the advent of ATO e-audits

In today’s electronic environment, the ATO can use computer assisted verification techniques to analyse records – especially when dealing with typical compliance “tick the box” number checking. The ATO can interrogate a taxpayer’s computer accounting system so great care must be taken when inputting data to that system; income and tax deductions must be correctly categorised and coded.

Verifying the correctness of tax consulting advice (i.e. deciding whether an interpretation of the tax or superannuation law is correct or not) cannot be effected through ATO e-audits because the giving of tax or superannuation law advice requires a detailed consideration of the taxpayer’s circumstances and then applying the laws to those circumstances; this is not a “one size fits all” pre-fabricated checkbox process.

At Nexia we pride ourselves in understanding our clients’ circumstances and in giving tailored advice – we do not regurgitate out of the box-pre-fabricated solutions – after all, advice relevant to one client may not be applicable to another client’s individual circumstances.

14 FEBRUARY 2018

Are you entitled to claim fuel tax credits?

Please ensure that fuel tax credit (FTC) claims are made at the correct rate because the fuel tax credit rates have increased from 5 February 2018. FTCs are calculated on the amount of fuel tax payable and the type of fuel (petrol, diesel, kerosene, blended fuels) used. FTCs are available for vehicles with a gross vehicle mass exceeding 4.5 tonnes that travel on public roads. FTCs may also be available for eligible business usage of machinery, plant, equipment and light vehicles travelling off public roads or on private roads. Simplified fuel tax credit rules apply for claims of less than $10,000.

We would be pleased to assist with making FTC claims as well as reviewing whether correct rates for claiming FTCs have previously been used.

15 NOVEMBER 2017

Can you be released from your tax debts?

The ATO can release individual taxpayers from their tax debts if the payment of the tax debt would expose such individuals to serious hardship (i.e. because of the payment of the tax debt, the individual would no longer be able to provide food, accommodation, clothing, medical treatment and education for the individual or their family).

However, the ATO cannot release a taxpayer’s tax debt if the taxpayer is already in serious financial trouble before the tax debt arises.

Furthermore, a trustee of a deceased estate may apply for the release of the deceased’s tax debt if payment of the tax debt would cause serious hardship for dependants of the deceased estate.

8 NOVEMBER 2017

Single touch payroll compulsory from 1 July 2018 if you have 20 or more employees

The Single Touch Payroll (STP) system will be compulsory from 1 July 2018 for all employers that have 20 or more employees at 1 April 2018.

Pursuant to the STP system, employers will need to report payments such as salaries and wages, pay as you go (PAYG) withholding and superannuation information directly to the ATO at the same time they pay their employees.

Furthermore, information reported through STP will be pre-filled into business activity statements (e.g. employers will no longer be required to provide payment summaries to individuals or a payment summary annual report to the ATO).

Please talk to us (especially if you would likely have 20 or more employees at 1 April 2018) so that we can assist you to transition to STP (i.e. to assist you to align the reporting of PAYG and superannuation contributions to the payroll process) and to ensure your systems are capable of STP reporting.

8 NOVEMBER 2017

ATO spotlight on certain not-for-profit (NFP) activities

The ATO is concerned that some NFP entities dishonestly claim tax concessions or refunds to which they are not entitled.

In particular, NFP entities that do not lodge their returns on time or incorrectly claim FBT rebates and exemptions may be subject to ATO investigations. Also, NFP entities that do not apply their income and assets solely for a charitable purpose may lose their tax exempt status.

Although a NFP may not have been involved in any of such activities, we are obliged to alert you about the increase in ATO scrutiny on NFP activities. We can assist you to review your organisation’s status as a NFP as well as the information you provide in tax returns and activity statements – and if you have made a mistake – assist you in making a voluntary disclosure.

1 NOVEMBER 2017

Mutuality and not-for-profit organisations

Taxable not-for-profit (NFP) organisations (e.g. certain social clubs, certain business and professional bodies and sporting clubs that are not tax-exempt) use the principle of mutuality to calculate their taxable income.

Mutuality basically means that an organisation cannot derive income from itself and therefore any surplus arising from contributions of members to a common fund will not be assessable income – however income derived from sources outside the group will still be assessable income (e.g. sponsorship and certain grants, proceeds from selling souvenirs to non-members and fees received for advertising in the organisation’s magazine)

Please contact us if your NFP organisation needs to lodge income tax returns and pay income tax. We can help you prepare your income tax return based on the mutuality principle and provide advice about the different concessional tax rules that are available to NFPs.

18 OCTOBER 2017

Further ways to protect yourself against tax scams

Last week we provided tips on what to do when someone purporting to be from the ATO contacts you by telephone.

However, in today’s interconnected world, information you share online must be protected to prevent scammers impersonating you. With cybersecurity threats becoming an everyday occurrence, you should ensure that your staff and clients keep their personal information (e.g. user IDs, passwords, TFNs) secure and that they do not indiscriminately click on downloads, hyperlinks or open attachments in unsolicited or unfamiliar emails, SMS or social media.

Sharing too much personal information on social media may also put a person at risk of targeted attacks – therefore, ensure social media profiles are set to private and be cautious about which friend requests to accept.

Please speak to us if you are interested to hear about further ways you can safeguard your business against cybersecurity risks and how to recognise scam emails pretending to be from the ATO.

18 OCTOBER 2017

Outstanding tax debt? We can help you set up a payment plan

We would strongly encourage any business with current outstanding tax debts to engage with your Nexia representative to ensure outstanding tax debts are paid in a timely and affordable manner. We can assist a business in establishing a payment plan with the ATO to avoid or minimise penalties and late interest charges on outstanding tax debts, or alternatively your Nexia representative can arrange solutions to refinance and restructure your debts, in order to manage your cashflow.

While having an ATO payment plan, you still need to lodge all of your ongoing activity statements and tax returns on time and the ATO will expect tax liabilities arising from those lodgements to be paid.

11 OCTOBER 2017

What to do when the ATO contacts you

If you are contacted by the ATO, you are within your rights to advise the ATO officer that Nexia is your tax agent and that you would prefer their assistance with any responses to the ATO. Successive Court decisions have authorised this approach provided the response to the ATO is undertaken with a reasonable timeframe, usually within 14 days – this can be extended in appropriate circumstances.

Please also be wary of people claiming to be from the ATO and making enquiries about your business or your employees. Unless the person can present a valid ATO authority (called a warrant card), no responses should be given to the person who could be anyone from a private investigator, family lawyer or general fraudster.

Determining whether the person is an ATO officer is even more difficult when the alleged ATO person is making enquiries over the telephone. Your first line of defence is to ask the person to contact your Nexia advisor regardless of how urgent the purported ATO person says their enquiry is. Such demands are usually a “try-on”. Further, a legitimate ATO officer is usually pleased to advise you of the ATO general switchboard telephone number to ring and the relevant officer’s extension number – we recommend that you give that number to your Nexia advisor in order for them to contact the ATO officer.

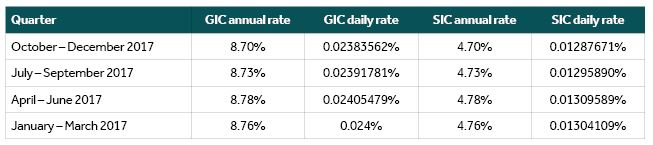

20 SEPTEMBER 2017

What is the difference between GIC and SIC?

The ATO charges interest on unpaid tax debts and shortfall amounts. A shortfall amount is the difference between the amount of tax originally assessed and the increased amount of tax assessed resulting from the issue of an amended assessment by the ATO.

- The lower shortfall interest charge (SIC) rate will be charged on any increased tax debt for the period leading up to amendment of an assessment;

- In contrast, the higher general interest charge (GIC) rate will be charged on any tax debt that remains unpaid after the assessment was amended.

The rates at which GIC and SIC are imposed differ from quarter to quarter as set out in the table below:

GIC will therefore apply to the original assessments and to any tax shortfalls (as evidenced by amended assessments) and associated SIC from their due date if they are not paid by that date.

Both the GIC and SIC accrues daily and is deductible for tax purposes in the year the taxpayer receives a notice of amended assessment.

Please speak to us if you have tax debt outstanding as we may be able to negotiate a remission of GIC or SIC on your behalf.

23 AUGUST 2017

Single touch payroll is here

Businesses may start using the new Single Touch Payroll (STP) system from 1 July 2017 (from 1 July 2018, STP will be mandatory for all employers that have 20 or more employees at 1 April 2018.

Some benefits of adopting the STP system are:

- employers will be able to report salary or wages, pay as you go (PAYG) withholding and superannuation information directly to the ATO at the same time they pay their employee; and

- reporting obligations will be streamlined because information reported through STP will be pre-filled into business activity statements (e.g. employers will no longer be required to provide payment summaries to individuals or a payment summary annual report to the ATO).

Employees who have just started a new job would also be able to complete their tax file number (TFN) declaration and Superannuation Standard Choice forms online using myGov or they can still use the existing paper process.

Please come and talk to us so that we can assist you to transition to STP (i.e. to assist you to align the reporting of PAYG and superannuation contributions to the payroll process) and to ensure your systems are capable of STP reporting.

9 AUGUST 2017

What to do if the ATO imposed a penalty on you?

The ATO can impose fixed administrative penalties on taxpayers that make false or misleading statements on their tax returns that result in under paid tax. For example, if a person claims excessive deductions to which they are not entitled or do not declare all income they have earned they may pay insufficient tax.

The amount of the penalty is fixed depending on the amount of “culpability” the taxpayer exhibited when filling in the tax return:

- 25% of the shortfall amount for taxpayers failing to take reasonable care (e.g. did not act like a reasonable person when completing your tax return);

- 50% of the shortfall amount for taxpayers acting recklessly (e.g. suspected that there would be real risk of a shortfall amount arising in your tax return but disregarded this risk); or

- 75% of the shortfall amount for taxpayers acting with intentional disregard of the law (e.g. fully aware of the clear tax obligation but disregarded the obligation)

Please contact us if you have been subject to such a penalty so that we can assist you in dealing with the ATO. We may be able to have your penalty remitted in full or partly depending on your circumstances (e.g. your compliance history and whether tax was deferred or avoided).

2 AUGUST 2017

Beware of tax scams

Taxpayers should keep their personal information (e.g. tax file number, bank account information and date of birth) secure and not disclose that information with anyone purporting to be from the ATO.

A current scam involves taxpayers receiving phone calls (where ATO telephone numbers appear in the caller ID) that threaten the taxpayers with arrest or jail if money is not paid into certain bank accounts or tax debts are not settled with gift of iTunes cards. Regrettably, many elderly and disadvantaged people react in fear and give the caller their personal information including access to their bank accounts or credit cards.

The ATO is investigating these bogus phone calls and asks that taxpayers take as many details as possible from the caller in order that such information may be given to the ATO. If you or someone you know has fallen victim to a tax scam, please contact us so that we can report the scam to the appropriate people in the ATO.

19 JULY 2017

No failure to lodge penalty if lodge outstanding returns by 31 August 2017

In acknowledgement of the ATO’s frequent electronic system maintenance issues, taxpayers now have until 31 August 2017 to lodge the following documents without incurring failure to lodge (FTL) penalties:

- 2016 tax returns;

- November 2016 to July 2017 monthly activity statements; and

- Quarter 2 and Quarter 3 2017 PAYG instalment activity statements and quarterly activity statements.

It is understood that if a FTL penalty has been imposed previously in respect of any of these outstanding documents, the ATO will automatically remit the FTL penalty (i.e. without the taxpayer having to apply for a remittance).

Please contact us if you have been affected and the ATO does not automatically refund your FTL penalty.

21 JUNE 2017

Streamlined reporting with Single Touch Payroll

The new Single Touch Payroll (STP) system whereby employers will be able to report salary or wages, pay as you go (PAYG) withholding and superannuation information directly to the ATO at the same time they pay their employees, will have a soft/voluntary start date of 1 July 2017 (from 1 July 2018, STP will be mandatory for all employers that have 20 or more employees – as measured at 1 April 2018).

The STP system will therefore streamline reporting obligations because information reported through STP will be pre-filled into business activity statements. Employers will no longer be required to provide payment summaries to individuals or a payment summary annual report to the ATO.

Please come and talk to us so that we can assist you to transition to STP (i.e. to assist you to align the reporting of PAYG and superannuation contributions to the payroll process) and to ensure your systems are capable of STP reporting.

31 MAY 2017

Do you know all the concessions that not-for-profit organisations are entitled to?

An eligible not-for-profit (NFPs) organisation may be entitled to claim certain tax concessions (e.g. FBT rebates and exemptions, GST concessions and income tax exemption).

These tax concessions are available if certain requirements are met (e.g. the NFP must be endorsed by the ATO to qualify for a certain concession)

Our reviews of many NFP organisations have found that the concessions in the FBT and GST laws are not being properly claimed resulting in excessive tax costs. Some NFPs are not claiming their rightful tax exemption and others are incorrectly claiming tax exemption. These incorrect applications of the tax laws often occur when staff are replaced or incorrect instructions are passed on to new staff or the new staff simply do not understand the “hand-over”.

Our initial “safety check” reviews may not come at a significant cost and invariably are significantly less than penalties and interest that otherwise would be charged by the ATO following their audit.

Please contact your Nexia advisor if you would like us to undertake a “safety check” review. We are always pleased to give you a non-obligation quote.

17 MAY 2017

Beware of tax scams when using social media

The ATO is warning taxpayers to be careful of what information they share on social media, particularly because scammers may use that information to impersonate such a user of social media and send scam emails, SMS or social media messages purporting to be from the user.

With cybersecurity threats becoming an everyday occurrence, you should ensure that your staff and clients keep their personal information (e.g. user IDs, passwords, TFNs) secure and that they do not indiscriminately click on downloads, hyperlinks or open attachments in unsolicited or unfamiliar emails, SMS or social media.

Please speak to us if you are interested to hear about further ways you can safeguard your business against cybersecurity risks and how to recognise scam emails pretending to be from the ATO.

11 MAY 2017

Tax treatment of insurance proceeds

Recently Nexia Australia assisted a client who owned a rental property that suffered considerable flood damage. Because the property was insured, the client received insurance proceeds.

Our job was to determine how the insurance proceeds would be treated for tax purposes.

Broadly, the taxation treatment of insurance proceeds depends on what the insurance cover is for. For example, if the insurance proceeds were received:

- to cover the cost of repairs to the rental property – the proceeds will only be assessable income in the income year in which the repair expenditure is incurred (i.e. the proceeds will not be assessable income in the year of receipt if no repairs have been effected)

- as compensation for lost trading stock – the proceeds will be assessable income as ordinary income (because buying and selling trading stock as well as insuring such trading stock is part and parcel of business activities)

- as compensation for the destruction of depreciating assets – a balancing adjustment event will occur and the proceeds will form the termination value of the destroyed depreciating asset.

- If the termination value exceeds the adjustable value (i.e. broadly the depreciated value of the asset) – the difference would be included in assessable income; and

- If the termination value is less than the adjustable value – the difference will be tax deductible.

- as compensation for the loss of capital works – the proceeds will be capital in nature (but will not be assessable income because no deduction is available for the loss of capital works)

Please speak to your Nexia adviser if you have recently received insurance proceeds and are unsure of the correct taxation treatment.

22 MAR 2017

Building & construction businesses and overdue taxable payments annual reports

As mentioned in an earlier Top Tax Tips, taxpayers operating in the building and construction industry had until 29 August 2016 to lodge their taxable payments annual reports (i.e. reports that detail the total payments made to contractors during the year ended 30 June 2016) with the ATO.

If you failed to lodge your taxable payments annual report by the due date, please contact us so that we can lodge the annual report on your behalf as soon as possible as well as negotiate a remission of penalties with the ATO.

If you have received a final reminder letter from the ATO, please note that lodgement will be due 21 days from the date of issue of the letter.

For more information on the taxable payments annual reports, please see our specific article dealing with this issue.

8 FEB 2017

Claim fuel tax credits at the new rate that applies from 1 February 2017

Please ensure that fuel tax credit (FTC) claims are made at the correct rate because the fuel tax credit rates have increased from 1 February 2017. FTCs are calculated on the amount of fuel tax payable and the type of fuel (petrol, diesel, kerosene, blended fuels) used. FTCs are available for vehicles with a gross vehicle mass exceeding 4.5 tonnes that travel on public roads. FTCs may also be available for eligible business usage of machinery, plant, equipment and light vehicles travelling off public roads or on private roads.

We would be pleased to assist with making FTC claims as well as reviewing whether correct rates for claiming FTCs have previously been made.

9 NOV 2016

Building & construction businesses and overdue taxable payments annual reports

As mentioned in an earlier Top Tax Tips, taxpayers operating in the building and construction industry had until 29 August 2016 to lodge their taxable payments annual reports (i.e. reports that detail the total payments made to contractors during the year ended 30 June 2016) with the ATO.

If you failed to lodge your taxable payments annual report by the due date, please contact us so that we can lodge the report on your behalf as soon as possible as well as negotiate a remission of penalties with the ATO.

For more information on the taxable payments annual reports, please see our specific Nexia alert dealing with this issue.

Let us assist your registered charities to apply for funding

If you are a registered charity you may potentially be eligible to receive funding from various charitable trusts and endowments.

Please contact us if you would like us to explore different funding opportunities that may be available for you.

19 OCT 2016

Developers of retirement villages: Can they claim their input tax credits?

A recent Administrative Appeals Tribunals (AAT) decision may affect developers of retirement villages to claim GST credits on the development costs (e.g. the costs of acquisition of the land and for the construction of the retirement village).

The AAT rejected a developer’s claim for input tax credits on 91% of such development costs on the basis that the retirement village predominantly makes input taxed supplies (e.g. units are rented or licenced) as opposed to making taxable supplies by selling the units.

This decision serves as a warning for developers and may discourage some because they would no longer be able to claim GST input tax credits on total development costs.

This is only one of the issues affecting the aged care sector – please see our Aged Care and Retirement Living Capability Statement to discover more ways we can help you with your retirement needs as well as more comments on the implication of this case on the Nexia website and in the Australian Property Journal.

5 OCT 2016

Ancillary funds registered as charities – only needs to report to the ACNC

Ancillary funds registered as charities now only need to report their 2016 annual return to the Australian Charities and Not-for-profits Commission (ACNC) by 28 February 2017.

Ancillary funds not registered as charities must continue reporting to both the ATO and ACNC.

14 SEP 2016

Mineral exploration companies - take action before 30 September 2016 for incentive

Small Australian mineral exploration companies that want to participate in the exploration development incentive program (i.e. an incentive to attract more investments in such companies) must, by 30 September 2016, lodge their exploration development incentive participation form to notify the ATO of their estimated 2016 exploration expenditure and estimated tax loss.

Please contact us if you are interested in partaking in the exploration development incentive program or need some assistance in preparing and lodging the application form.

This is only one of the issues affecting the mining sector – please see our Mining, resources and energy capability statement to discover more ways we can help.

28 SEP 2016

Charities – Ensure your annual reporting is up to date

Charities that have still not submitted their outstanding annual 2015 information statements (originally due by 31 January 2016) will have a red mark struck against their name on the public Charity Register listing (because they are more than 6 months overdue with their annual reporting).

To prevent such naming and shaming (i.e. having such a red mark may influence a donor’s decision whether or not to donate money to such a charity), the red mark can be removed when the charity submits its information statement. In extreme cases where there has been no reporting for 2 years, such charities may lose their tax-exempt status.

Please contact us if your charity needs assistance submitting its annual information statement.

This is only one of the issues affecting the not-for-profit sector – please see our Not-for-profit capability statement to discover more ways we can help.

Are you a farmer affected by drought?

The ATO is offering assistance to primary producers affected by drought (e.g. giving them extra time to pay their taxes, waiving penalties or interest on late payments, offering payment plans as well as interest free periods and in cases of serious hardship, release such farmers from payment of some taxes).

If you are a farmer, please speak to us so that we can help you manage your tax obligations.

Building & construction industry – act now if you have outstanding tax debts

The ATO has warned that they will take action against contractors in the building and construction industry that have outstanding tax debts.

In worst case scenarios, the ATO may issue a garnishee notice (i.e. where the ATO may collect an outstanding tax debt by taking money from the bank account of a contractor who owes money to the taxpayer who has the outstanding tax liability).

Please contact us if you are working in the building and construction industry and are falling behind with your tax debts. We can work with you to establish a sensible repayment plan with the ATO.

31 AUG 2016

Retirement village operators may deduct capital growth payments made to outgoing residents

The ATO confirmed that, from 26 November 2014, capital growth payments made to an outgoing resident (i.e. broadly the difference between the initial entry price paid by the outgoing resident and the entry price paid by the new resident) will be revenue in nature and therefore deductible to the retirement village operator.

However, any such payments made before 26 November 2014 (i.e. the date the ATO issued an Addendum to their original tax ruling dealing with this issue), could either be treated as:

- capital – i.e. then such a payment would not be deductible; or

- revenue – i.e. then such a payment would be deductible.

This is only one of the many issues affecting the aged care and retirement living sector in Australia – please read our Aged Care and Retirement Living Capability Statement to discover more ways we can help you with your retirement needs.

10 AUG 2016

Building & construction businesses to report payments made to contractors by 29 August 2016

The ATO has reminded taxpayers operating in the building and construction industry to lodge their Taxable payments annual reports, detailing the total payments made to contractors in 2016, with the ATO by 29 August 2016 (usually such reports must be lodged by the 28th of August each year, but since that date is a Sunday this year, the report can be lodged on Monday, 29 August 2016). Penalties may apply if such reports are not lodged by the due date.

Please contact your Nexia adviser so that we can help you fill in your report as well as lodge it for you on time.

Further information on this Taxable payments annual report is available on nexia.com.au