"We're open for business!"

Major banks and financial institutions can be quick to make that promise. However, plans could take a turn when it comes to borrowing funds or rolling over existing facilities.

That's because risks vary throughout industries, and they evolve from year to year — especially in Australia’s dynamic wine industry. As banks become more careful in reassessing associated risks, wine businesses are called to up their financing strategies.

This can be tough, but it is possible. The gross value of wine grape production is forecasted to rise by 11% (up to $834 million) in 2023-2024. Meanwhile, global demand is expected to rise as inflation falls and economies recover.

In other words, funding opportunities are on the horizon. The question is, how do you work towards them?

If you're in the wine industry looking for funds — here are 7 key tips for borrowing and refinancing your wine business.

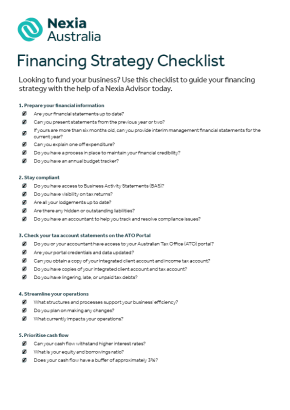

1. Prepare your financial information

Are your financial statements up to date?

To better your chances at financing, you'll need updated financial statements. Be sure to present statements from the previous year or two. If yours are more than six months old, consider providing interim management financial statements for the current year.

If you want to go the extra mile, you'll also need an explanation. Highlight any expenditures that could deter banks and reassure them that these are one-offs. Showcase the steps you've taken to address past issues and emphasise a bright future. Even better, you can provide annual budgets so you and your lender can track results together.

Remember, banks prefer successful, profitable businesses. Having updated financial statements will reflect that.

2. Stay compliant with Business Activity Statements (BAS) and tax returns

Are all your lodgements up to date?

If not, then it's time to get things organised. The great news is that Nexia’s accountants and advisors can help you track, resolve, and prevent compliance issues.

Lenders want to know that your business is on top of statutory obligations. They'll be on the lookout for any hidden or outstanding liabilities.

By demonstrating due diligence, you reassure lenders of your business' integrity and commitment. This gives you a better chance at getting funding.

3. ATO Portal: Check your tax account statements

Do you or your accountant have access to your Australian Tax Office (ATO) portal?

If not, make sure to update your credentials and can get access to your data. Access to your portal will come in handy for ATO-related transactions in the future.

In this case, be sure to obtain your tax account statements. You will need to provide copies of your integrated client account and income tax account. This tells banks that you have no lingering debt. Remember, any late or unpaid tax debt could affect your chances of refinancing.

After all, banks prefer businesses with a clean record. With clean tax accounts you reinforce your credibility that you can manage your finances.

4. Streamline your operations

Have you streamlined your business operations?

Be upfront about your business operations. Highlight the structure and processes that support your business' efficiency.

Bonus tip — if you plan on making any changes, make it a point to inform your lender. Be transparent about anything that impacts your operations from the get-go.

The bottom line here is that banks don't like surprises. A well-structured business that communicates well speaks of stability.

5. Prioritise cash flow

Can your cash flow withstand higher interest rates?

Many businesses make the mistake of biting off more than they can chew. Before borrowing, ensure you have an allowance for higher interest rates.

Having a large equity compared to your borrowings is one thing. However, your cash flow must withstand higher interest rates plus a buffer of approximately 3%.

By optimising your cash flow, you set your business up for more opportunities. This includes funding and refinancing.

6. Prepare for a lengthy process

Are you prepared to play the long game?

Funding can take 3–4 months at the minimum. Meanwhile, reorganisation can take up to 6 months, even more. Do you have the resources to make it through the timeline?

If your current lender is not as acceptable as they used to be, explore other options. Try connecting with different lenders. With expert advice and realistic feedback from accountants, there’s no need to panic.

Sticking to a realistic timeline protects your business and keeps you on track.

7. Connect with industry experts

Do you have enough knowledge of the funding process? Are there specific questions you need clarity on?

Many businesses underestimate the complexity of funding. Connecting with Nexia’s many experts who can give you tailored solutions based on your needs will go a long way.

There’s no one-size-fits-all approach to financing. With our Nexia expert advisors in your corner, you can access game-changing insights you wouldn't have considered without them.

This helps you better understand your financial situation and could make the most difference in securing your funding.

What’s next?

The financial landscape is always changing, but this is your opportunity to get to know your business on a deeper level.

More than just applying for funding and presenting documentation, you’re in a unique position to spot any blind spots, streamline processes, optimise resources, and explore various opportunities.

With lenders becoming more selective, preparing for any funding delays ahead of time and asking the right questions can make all the difference.

Connect with a Nexia Advisor and uncork your funding potential today!